Explore our network of country and industry based websites to access localized information, product offerings, and business services across our group.

Log in to start sending quotation requests for any product.

Don't have an account? Sign Up Here

Home Asia Cocoa Powder Supply 2026 in West Africa

Trade Insights | Supply Chain | 22 April 2026

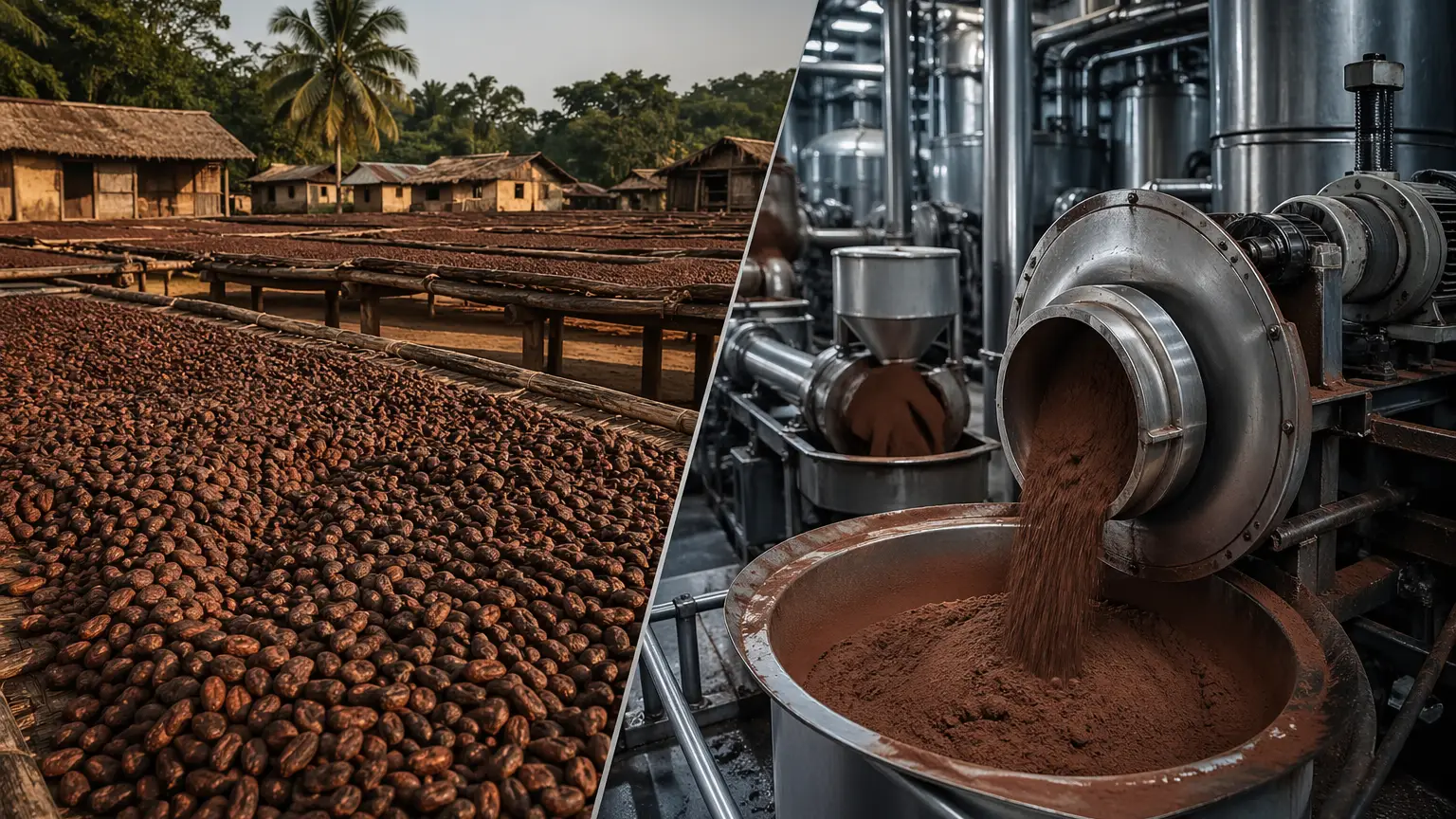

West Africa — led by Côte d'Ivoire and Ghana — supplies approximately 70% of the world's cocoa beans, which Asian processors grind into cocoa powder at facilities in Malaysia, Indonesia, and China. Cocoa powder shipped from Abidjan and Tema to Asian buyers travels 25–30 days via container through the Strait of Malacca, with freight costs rising 20% in Q1 2025 amid port congestion. Asian buyers cannot fully replace West African origin by 2026, but Ecuador, Indonesia, and Brazil offer credible partial substitutes that procurement teams should now qualify as secondary suppliers.

Cocoa powder is produced by pressing cocoa liquor (ground cocoa beans) to extract cocoa butter, then grinding the remaining cocoa cake. The result is either natural cocoa powder (pH 5–6, lighter color) or alkalized (Dutch-processed) cocoa powder (pH 7–8, darker, more soluble), the latter being the dominant commercial form used in chocolate beverages, bakery mixes, and confectionery across Asia.

The reason West Africa dominates starts at the bean level. Côte d'Ivoire and Ghana together supply over 60% of the world's cocoa beans, according to ICCO data, and their forastero-variety beans — while not specialty grade — deliver consistent fat content and fermentation characteristics suited to large-scale powder production. Asian processors in Malaysia, Indonesia, and China import these beans, grind them domestically, and either use the resulting powder in their own manufacturing or export it across the region.

The key quality specification most buyers in Asia track is fat content (10–12% for low-fat powder, 20–22% for high-fat) and alkalization level, measured by pH. West African beans reliably produce mid-range fat profiles, making them the default input for regional powder production. Fine-flavor origins from Ecuador or Peru produce distinctly different flavor profiles better suited to premium applications than to standard food manufacturing.

West African dominance is not just significant — it is structurally extreme.

| Country | 2024/25 Production Est. (MT) | Global Share (%) | Trend |

|---|---|---|---|

| Côte d'Ivoire | ~1,300,000 | 28% | Declining |

| Ghana | ~480,000 | 10% | Sharply declining |

| Nigeria | ~280,000 | 6% | Stable |

| Cameroon | ~240,000 | 5% | Stable |

| West Africa Total | ~2,300,000 | ~49–52% | Declining |

| Ecuador | ~350,000 | 7% | Growing |

| Brazil | ~270,000 | 6% | Growing |

| Indonesia | ~200,000 | 4% | Stabilizing |

| Other Americas/Asia | ~300,000 | 6% | Growing |

| Global Total | ~4,700,000 | 100% |

Sources: ICCO November 2025 Bulletin; ICAO estimates vary; figures are approximate.

Côte d'Ivoire's Conseil du Café-Cacao (CCC) projected 2025/26 main crop production at only 1.3 million tonnes, down from 1.7 million tonnes three years prior. Ghana's harvest, which once exceeded 1 million tonnes annually, fell below 500,000 tonnes in the most recent season due to a combination of black pod disease (Phytophthora palmivora), excessive rainfall during pollination, and an aging tree base. The average age of cocoa trees in Ghana now exceeds 30 years, well past peak productivity.

The production decline in West Africa since 2022 drove cocoa prices from approximately $2,500/MT in early 2023 to a peak of $11,530/MT in June 2024 — the highest price in 60 years, per London terminal data. By October 2025, prices had corrected to approximately $4,000/MT as supply partially recovered, but they remain more than 50% above their decade-long average. For Asian cocoa powder buyers, that feedstock cost spike translated directly into manufactured product cost increases of 30–60%, depending on contract timing.

What makes the West African contraction commercially significant for Asian buyers is that it is structural, not cyclical. Aging tree stocks cannot recover quickly. The Ivorian CCC acknowledged in December 2025 that returning to prior production levels requires significant reinvestment that will take several years to materialize. Buyers who treat this as a temporary disruption and return to single-origin West African procurement risk repeat exposure to the same price and availability shock that hit the market in 2023–2024.

Asia-Pacific is simultaneously the world's largest cocoa powder processing region and one of its most dependent on West African raw material. The structure requires close examination.

| Country | Cocoa Powder Production (2024, MT) | Asia-Pacific Share (%) |

|---|---|---|

| China | ~469,000 | ~36% |

| Malaysia | ~214,000 | ~16% |

| Indonesia | ~135,000 | ~10% |

| Other Asia-Pacific | ~512,000 | ~38% |

Source: IndexBox Asia-Pacific Cocoa Powder Market Report, 2025.

China dominates production volume, primarily serving its own domestic confectionery, beverage, and bakery markets. Malaysia is the region's largest exporter, shipping approximately 200,000 MT of cocoa powder in 2024, with Malaysia's Guan Chong Berhad, JB Cocoa Sdn Bhd, and the local operations of Barry Callebaut and Cargill collectively operating the largest grinding capacity in Southeast Asia. Indonesia, historically the world's third-largest cocoa bean producer, processes beans at facilities operated by Barry Callebaut Comextra Indonesia and PT Cargill Indonesia, primarily in Makassar and Gresik.

Malaysian and Indonesian processors depend on West African bean imports for the majority of their grinding inputs. Malaysia produces negligible cocoa domestically and imports virtually all its bean supply. Indonesian domestic bean production of approximately 200,000 MT covers only a portion of its grinding capacity, with the remainder sourced from Côte d'Ivoire, Ghana, and increasingly Ecuador.

This means that when West African supply tightens, the entire regional processing chain is exposed simultaneously: bean prices rise, grinders face margin compression, and finished cocoa powder prices increase for downstream buyers across China, India, Japan, and Southeast Asia. The 2023–2024 price shock moved through exactly this mechanism.

Cocoa beans and processed cocoa powder follow distinct logistics routes to Asia. Buyers need to understand both.

Raw cocoa beans move from Abidjan (Port of Abidjan and Port of San-Pedro) and Tema (Ghana) by container or break bulk vessel. Transit times to Malaysian and Indonesian processing ports run 25–30 days via the Cape of Good Hope route, or 20–25 days via the Suez Canal. Since the Red Sea disruptions that began in late 2023, most carriers have defaulted to the Cape route, adding 7–10 days to transit times and approximately 15–20% to freight costs.

Finished cocoa powder exported from Malaysia (primarily from Port Klang and Penang) to buyers in China, India, Japan, and Australia travels 3–15 days depending on destination. The short intra-regional leg is the supply chain's most reliable component.

In Q1 2025, wait times at the Port of Abidjan reached 14 days for container loading, driven by volume surges at the start of the main crop season. The CCC introduced truck volume restrictions in December 2025 to control congestion, capping daily unloading per factory based on capacity — a measure that reduced wait times but constrained throughput. Buyers relying on just-in-time inventory models for West African-origin beans must account for this seasonal port risk, particularly during October–March, which corresponds to the Ivorian main crop harvest.

Cocoa beans are shipped in 60-kg jute bags or in bulk, requiring temperature and humidity monitoring to prevent mold (critical below 8% moisture content during transit). Cocoa powder is more stable and ships in 25-kg multi-ply paper bags, typically via dry container. Neither product requires refrigeration, but moisture control during loading at West African ports — where humidity frequently exceeds 80% — is a documented quality risk.

| Route | Origin Port | Destination | Transit Days | Key Risk |

|---|---|---|---|---|

| Beans to Malaysia | Abidjan / San-Pedro | Port Klang | 25–30 (Cape) | Port congestion, Abidjan |

| Beans to Indonesia | Tema | Surabaya / Makassar | 25–32 (Cape) | Red Sea diversion |

| Powder: Malaysia to China | Port Klang | Shanghai / Tianjin | 5–7 | Low |

| Powder: Malaysia to India | Port Klang | Nhava Sheva / Chennai | 8–12 | Low |

| Ecuador beans to Asia | Guayaquil | Port Klang | 22–27 | Routing complexity |

| Risk Dimension | Rating | Key Trigger |

|---|---|---|

| Concentration Risk | VERY HIGH | Côte d'Ivoire + Ghana = 60%+ of global beans |

| Geopolitical Risk | MEDIUM | CCC export/pricing policy; Nigerian instability |

| Climate Risk | HIGH | El Niño events; aging West African tree stock |

| Logistics Risk | MEDIUM-HIGH | Abidjan port congestion; Red Sea diversion |

| Structural Risk | HIGH | Sustained underinvestment in West African farms |

No commodity buyer should be comfortable with 60% of their raw material supply originating from two adjacent countries that share the same climate systems, the same disease pressures (black pod, swollen shoot virus), and similar farm infrastructure constraints. The 2023–2024 price surge demonstrated precisely what happens when both suppliers disappoint simultaneously. Asian buyers holding only West African-origin contracts had no practical alternative at speed: Ecuador could not scale up fast enough, and Indonesian domestic supply was already committed.

West African cocoa is produced almost entirely by smallholder farmers working plots of 2–5 hectares. These farmers have no irrigation and cannot hedge against weather. The El Niño weather pattern of 2023–2024 reduced soil moisture during critical pod development periods across both Côte d'Ivoire and Ghana. Agronomists expect climate volatility of this kind to recur with greater frequency. Average yields in West Africa have already fallen below 500 kg/hectare — half the yield achieved by well-managed agroforestry cocoa farms in Ecuador, which average approximately 800 kg/hectare.

The Ivorian government, through the CCC, controls farmgate cocoa pricing and export licensing. While it has not imposed outright export bans, CCC pricing decisions — particularly when they compress grinder margins — create temporary supply friction. Ghana's COCOBOD (Ghana Cocoa Board) operates similarly and has faced financial difficulties that delayed pre-financing to farmers, slowing 2023/24 crop mobilization. These institutional risks are less severe than a Chinese-style export restriction, but they introduce timing uncertainty that Asian buyers with tight production schedules cannot absorb without buffer stock.

The honest answer for Asian buyers considering supply diversification is that no single origin can replace West Africa at scale by 2026. But partial diversification is both achievable and commercially important.

Ecuador produced approximately 350,000 MT of cocoa in 2024, making it the world's fourth-largest producer and the largest in Latin America after Brazil. Between 2013 and 2023, LATAM-Caribbean cocoa production rose 56%, led by Ecuador, Brazil, and Peru, according to Statista data. Ecuador's productivity advantage is real: its agroforestry-grown Nacional/Arriba varieties yield approximately 800 kg/hectare versus sub-500 kg/hectare in West Africa.

For Asian buyers, the practical constraint is that Ecuadorian beans are predominantly fine-flavor (Arriba designation), making them more expensive than West African bulk varieties and primarily suited to premium applications. However, Ecuadorian CCN-51 hybrid varieties, which produce a bulk-grade commodity bean, are increasingly available and compatible with standard cocoa powder production. CFR Port Klang pricing for Ecuadorian CCN-51 runs approximately 10–15% above Ivorian beans, a premium that procurement teams should model as an insurance cost against supply disruption.

Transit from Guayaquil to Malaysian processing ports takes 22–27 days, slightly shorter than the West Africa-Cape route currently in use.

Indonesian domestic cocoa bean production stabilized at approximately 200,000 MT in 2024 after a period of decline from a peak of approximately 450,000 MT in 2012. The Sulawesi-grown Lindak variety is processed locally by Barry Callebaut, JB Cocoa, and PT Cargill Indonesia. For processors in Indonesia sourcing locally, this origin eliminates maritime logistics entirely. For processors in Malaysia or China, Indonesian beans offer a regional alternative to West Africa but at volumes insufficient to replace Ivorian supply on their own.

The Indonesian government has indicated intentions to expand farm rehabilitation programs, with gradual production increases expected toward 2030. Buyers with long planning horizons should track Indonesian supply as a medium-term diversification lever, not an immediate substitute.

Brazil produced approximately 270,000 MT in 2024 and is growing. However, its cocoa is predominantly destined for domestic consumption and high-value specialty export. Bahia-state cocoa, Brazil's main commercial variety, requires origin qualification and tends to command premiums that push it outside standard cocoa powder cost structures. Peru's output remains below 150,000 MT and is similarly premium-oriented.

| Origin | 2024 Production (MT) | Quality Grade | Suited for Bulk Powder | Transit to Malaysia |

|---|---|---|---|---|

| Côte d'Ivoire | ~1,300,000 | Bulk forastero | Yes | 25–30 days (Cape) |

| Ghana | ~480,000 | Bulk (premium quality) | Yes | 28–32 days (Cape) |

| Ecuador (CCN-51) | ~180,000 est. | Bulk hybrid | Yes | 22–27 days |

| Ecuador (Arriba) | ~170,000 est. | Fine flavor | Specialty only | 22–27 days |

| Indonesia | ~200,000 | Bulk Lindak | Yes | 3–5 days (local) |

| Brazil | ~270,000 | Semi-bulk / specialty | Partially | 30–35 days |

Cocoa beans account for 60–80% of the total cost of cocoa powder production, making this one of the most feedstock-sensitive commodities in the food ingredient space. When the London terminal cocoa price moves, powder prices follow within 4–8 weeks, the approximate lag of processing inventory cycles. The 2023–2024 crisis demonstrated this mechanism at its most extreme: beans that traded at $2,500/MT in early 2023 peaked above $11,000/MT by June 2024, and alkalized cocoa powder CFR Asia followed into record pricing territory.

Malaysia and Indonesia's major cocoa grinders operate on thin processing margins of $200–$400/MT over bean cost in normal markets. When bean prices spike, grinders with uncovered forward bean purchases face margin compression or losses. This can cause temporary reductions in grinder throughput, further tightening regional powder availability. The Q4 2024 margin squeeze at several Malaysian grinders temporarily reduced spot powder availability to Chinese and Indian buyers.

The November 2025 ICCO bulletin revised 2024/25 world production to approximately 4.698 million tonnes and indicated a small global surplus as the market rebalanced from the 2023/24 shortage. Prices corrected from the June 2024 peak of $11,530/MT to approximately $4,000/MT by October 2025. For April 2026, the market is trading in the $3,500–$4,500/MT range as the 2025/26 West African crop enters the mid-season assessment phase. The projected 10% output decline for 2025/26 from Côte d'Ivoire and Ghana will test how durable the current price correction proves.

Buyers should not interpret the correction from the 2024 peak as a return to pre-crisis norms. Structural underinvestment in West African farms means the supply recovery will be gradual and vulnerable to weather setbacks.

Most Asian buyers of cocoa powder purchase through one of four channels:

Direct from regional grinder. The largest volume channel for industrial buyers in China, India, and Southeast Asia. Buyers contract directly with Malaysian or Indonesian processors (Guan Chong, JB Cocoa, Barry Callebaut Malaysia, Cargill Indonesia) for term supply. This provides price certainty and CoA reliability but concentrates origin risk in West African-dependent processors.

International trading companies. Olam Food Ingredients (Singapore-based), Cargill, and ECOM Agroindustrial maintain origin purchasing networks across West Africa and Latin America. They can provide multi-origin contracts that blend Ivorian, Ecuadorian, and Indonesian-origin powder into a single supply program. This is the most practical route to origin diversification without the buyer establishing direct relationships in each origin country.

Regional distributors. Suited to mid-size buyers in Vietnam, Thailand, and the Philippines purchasing in 20–100 MT parcels. Distributors typically hold spot stock at bonded warehouses in Port Klang, Singapore, or Shanghai. Premium over direct grinder pricing is typically $100–$200/MT.

Spot market. Viable for small volumes and opportunistic purchasing but carries maximum price and availability risk during supply squeezes. Buyers who relied on spot procurement during the 2023–2024 crisis faced both price spikes and delivery delays simultaneously.

Given the structural production uncertainty in West Africa, buyers consuming more than 50 MT per month of cocoa powder should be on term contracts covering at least 60–70% of annual requirements. The 2023–2024 episode demonstrated that spot-reliant buyers faced not just higher prices but actual supply unavailability during peak shortage periods. Term contracts with a major grinder or trading house — ideally with multi-origin flexibility clauses — are the appropriate procurement posture for 2026.

For the balance of requirements, a secondary spot or short-term relationship with an Ecuadorian-origin supplier provides practical diversification without requiring the buyer to commit to full term volumes from a less-established origin.

The combination of 25–30 day maritime transit from West Africa, seasonal port congestion in Abidjan (October–March), and structural supply uncertainty supports holding 8–10 weeks of forward stock for buyers in China and India, and 6–8 weeks for buyers in Southeast Asia. This is a meaningful increase from the 4–6 week norm before 2023, but it is the appropriate buffer given demonstrated supply chain fragility.

West Africa will remain the dominant origin for cocoa powder inputs to Asia through 2026 and beyond. Côte d'Ivoire and Ghana's combined production capacity is simply too large for Ecuador, Indonesia, and Brazil to replace at current scale. Buyers expecting a complete restructuring of origin dependency within 12–24 months will be disappointed.

What is achievable — and strategically necessary — is partial diversification. For Asian buyers, that means:

For Asian procurement teams currently running single-origin West African programs, the question is not whether to diversify — it is how quickly and with which origins to begin.

Q: Who are the largest cocoa powder producers supplying Asia-Pacific? A: China is the largest producer in Asia-Pacific at approximately 469,000 MT annually (approximately 36% of regional output), primarily for domestic use. Malaysia is the largest regional exporter, with approximately 200,000 MT exported in 2024 through processors including Guan Chong Berhad, JB Cocoa, and Barry Callebaut Malaysia. Indonesia is the third-largest regional producer at approximately 135,000 MT.

Q: How is cocoa powder transported from West Africa to Asia? A: Cocoa beans are shipped from the Port of Abidjan (Côte d'Ivoire) and Port of Tema (Ghana) via dry container or break bulk vessel. Since Red Sea disruptions began in late 2023, most carriers have rerouted via the Cape of Good Hope, adding 7–10 days to transit and approximately 15–20% to freight costs. Transit from West Africa to Malaysian processing ports now runs 25–30 days. Finished cocoa powder is then re-exported from Port Klang or Penang to buyers across Asia in 3–15 days depending on destination.

Q: What factors drive cocoa powder prices for Asian buyers? A: Cocoa beans represent 60–80% of cocoa powder production cost, making London terminal cocoa pricing (ICE London contract) the primary price driver. When bean prices move, powder prices follow within 4–8 weeks. Secondary drivers include Malaysian Ringgit and Indonesian Rupiah exchange rates (which affect grinder cost structures), and freight rates on West Africa-Asia routes. The 2023–2024 bean price surge from $2,500 to over $11,000/MT caused cocoa powder prices to reach historic highs.

Q: What are the main supply chain risks for cocoa powder buyers in Asia? A: Concentration risk is the primary structural risk: Côte d'Ivoire and Ghana together supply over 60% of global cocoa beans, and both are experiencing production declines driven by aging tree stock, climate variability, and underinvestment at farm level. When both origins underperform simultaneously — as occurred in 2023/24 — there is no short-term alternative at comparable scale. Secondary risks include seasonal port congestion at the Port of Abidjan (particularly October–March) and Red Sea logistics disruption extending Cape route transit times.

Q: Can Asian buyers realistically replace West African cocoa powder with other origins? A: Not at full scale in the near term. Ecuador is the most viable partial substitute, producing approximately 350,000 MT of cocoa beans in 2024, with CCN-51 hybrid varieties suitable for standard cocoa powder production at a premium of approximately 10–15% over Ivorian beans. Indonesia offers intra-regional supply for local processors, though at insufficient volumes to replace West African imports. Latin America as a whole accounted for approximately 20% of global production in 2024, and that share is growing — but replacing West Africa's 49–52% concentration requires structural investment over a decade, not a procurement cycle.

We're committed to your privacy. Tradeasia uses the information you provide to us to contact you about our relevant content, products, and services. For more information, check out our privacy policy.

English

English

Indonesian

Indonesian

简体字

简体字

العربية

العربية

Español

Español

Français

Français

Português

Português

日本語

日本語

한국어

한국어

Tiếng Việt

Tiếng Việt